My Portfolio And Why I Am More Likely To Add To My Sands China Ltd (HKG:01928) Long Position In The Near Future.

Summary

This article will be an introduction to my current portfolio (5/31/2015) and also why I find Sands China Ltd (HKG:01928) worthy of my hard earned money in the future. I have started investing in US equities just this January 2015.

Part 1:

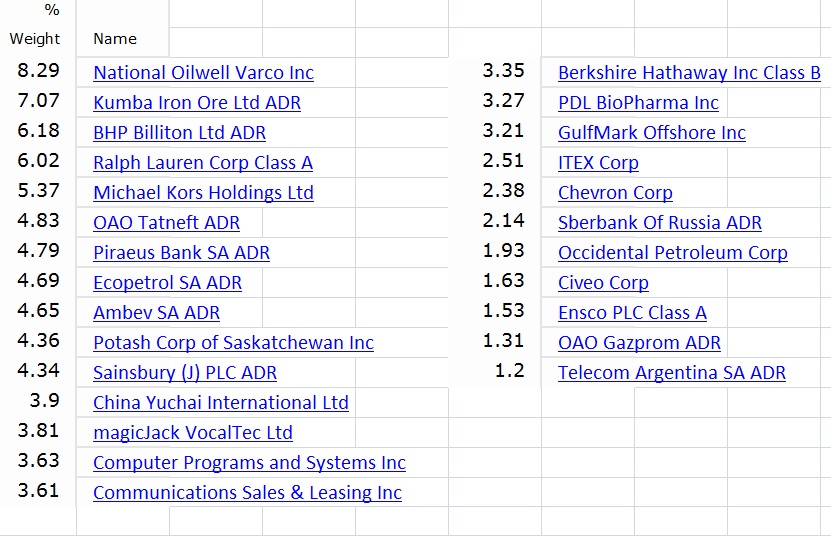

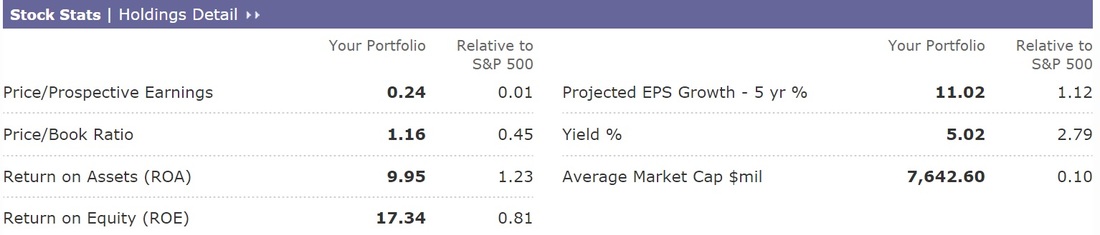

Using Morningstar's x-ray tool, this is my portfolio summary.

Summary

- My adventure in the world of investing.

- Sands China Ltd (HKG:01928) a possible buy.

- My valuation of Sands China Ltd reveals it is undervalued by 26.54%.

This article will be an introduction to my current portfolio (5/31/2015) and also why I find Sands China Ltd (HKG:01928) worthy of my hard earned money in the future. I have started investing in US equities just this January 2015.

Part 1:

Using Morningstar's x-ray tool, this is my portfolio summary.

As you may observe, I do not have those stalwart companies (such as JNJ, PG, MCD, and countless others). This is because I tend to rely on what James Montier have said on his book Value Investing, that a portfolio having low PEs outperforms those portfolios that have the glamorous stocks or high PEs over a long period of time. Speaking about long term horizon, I want to have that holding period of more than two years per stock purchase.

The checklist that I follow prior to purchasing are: <0.50 DE ratio, increasing ROIC, >30 Operating Margin, Positive Cash Flow, increasing Book Value, >2% dividend yield, and <15 PE ratio. In addition, I would be purchasing a stock of a company undergoing a recession in its industry. As you have observed, most of the companies in my portfolio are in the energy and basic materials industry.

Following the aforementioned checklist is quite hard especially if I see that the stock is at its four-year low and still PE shows >15 (like RL). But, it can be also difficult to time the market. So instead of timing the market, I buy a share of a company the following day I have formed my conviction, and add up to it whenever it further falls down (catching a falling knife as one may say; such as what happened to my KORS, NOV, OAOFY, KIROY, BPIRY, and BHP).

Other investments here may appear uninteresting because of where the company's operation is situated. However, I can only buy a company only if it has better fundamentals and cheaper valuations. As an example, I bought more OAOFY shares compared to CVX in the midst of that 50% in oil price decline early this year.

On the other hand, BRK.B is an exception. As a big fan of Warren Buffett, I bought a single share early this January just to have that opportunity to attend the 50th annual meeting in Omaha, NE.

Other capital misuse in this portfolio is the one assigned in the ESV. I purchased ESV in the same period of that oil drop, but it was only late when I realized that the company had increasing DE ratio from 0.19 in 2005 to 0.70 in 2015 (latest quarter). An interesting fact I have recently found out from reading John Train's Money Masters is that Richard Rainwater, an investor legend, had formed this company during the 1980's. Regardless, I still consider this as a faulty investment that I am willing to keep for the long run given a small exposure of 1.53 weighting in my portfolio.

Part 2:

Now, in addition to this portfolio, I also maintain a separate portfolio in Hong Kong and the Philippines.

For Hong Kong and the Philippines, I have the following shares and corresponding weighting in my portfolio (a separate portfolio per country):

I carefully screened almost <1,000 companies in the HangSeng Index with the aforementioned screening criteria I have mentioned above and find these companies as my best results. I also read their annual reports, and I guess it is okay to mention here that I find Perfect Shape PRC Holdings Ltd the most candid. Regardless, it is late that I found out that sending money to Hong Kong and dealing with their complex taxation and commission fees that I am only left with 10% return (instead of <15%) since I started investing this January 2015 (same time as when I started investing in US and other Foreign equities).

Now, I find the ongoing crackdown on China's notorious big spenders temporary no matter how much publicity it gets. Continuous innovation to attract visitors such as the new casino project will still be ongoing (like the Parisian Macao at Cotai Strips, Macao "sometime" this 2016) and people (not only Chinese), but people around the Asian Region would still find Macao a wonderful tourist destination. Although there are only six licensed operators in the Macao Island who may operate the casino business, I find Sands China with the best fundamentals among its peers (see checklist above-of course with some exceptions). With 70.2% ownership by Las Vegas Sands (NYSE:LVS) I do not think LVS would let Sands China easily flop. Morningstar gave Sands China a four star with a narrow economic moat. According to Value Line, the recent plunge in Sands China brought down LVS's top line of about 25%. Despite this, they kept their 2018-2020 price projection of LVS in the $90-$130 a share versus its current market price of $50.90.

But my focus is still on the Sands China. The three challenges I find in this company in addition to the ongoing economic problem in Macao is its CEO succession, the ongoing lawsuit concerning an unfair dismissal of then former Sands China CEO Steven Jacobs, and the recent initiation of dividends.

I assume that a lawsuit can cause a lot and it may exacerbate the already struggling company, thus creating a perfect storm in the short term. First, Sheldon Anderson's age of 81 can be an alarming factor given his influence in both the LVC and Sands China operations. In addition, Edward M. Tracy, who was recently appointed as the Sands China's CEO in 2011, has decided to retire last March 7, 2015. He stated that there were no disagreements and only to serve as a consultant to the company then after. I am assuming the current interim president and executive director, Robert G. Goldstein, to be able to fulfill the CEO role anytime given his extensive experience in the casino-hotels business. I just find it interesting that in the midst of the allegations made by Steven Jacobs (former Sands China CEO) about Sheldon Anderson's approval of prostitution in his casino and blackmailing of high-ranking Macao officials (Crowe, 2015), which is ongoing for four and a half years already, Edward M. Tracy, appointed as Sands China CEO after Steven Jacobs departure, now retired at only the age of 62. Lastly, the company only started giving dividends in 2012. With this short dividend history with a 98.9 payout ratio ($1.71 billion USD according to its 2014 annual report) I am thinking whether or not to just rely on possible capital appreciation in the long term rather than on the attractive 6.18% it currently provides.

Alright, now I am going to use my valuation to see what is the fair value of Sands China. I average eight different models so as to obtain my own fair valuation of a company. To give better information on how I evaluate a company, here are some of the important data I use: Morningstar's key ratios, CAPM's method of determining the cost of equity, PE PBV PS average price, using only 2/3 (67%) analyst's dividend growth projections, using 2/3 of the company's current earnings power, using Hagstrom's five- and ten-year discount cash flow model, and using five, nine, and fifteen year (if applicable) dividend growth.

As you may observe, I value a stock based on their dividend history and growth. In this case, I am force to assume the reasonable growth of 21.37% forecasted by Yahoo Finance instead of the outrageous 752.80% forecasted by 23 analysts in The Financial Times. Let us remember that with the recent 2012 dividend issuance, the company has had a 22.37% dividend growth, a CAGR of 22.12%. In addition with the already north of 90 payout ratio, I personally do not think that this would be maintained for the long run or the payout ratio must at least be lessened to attain consistency.

Upon my calculation for the fair value of Sands China, I had to eliminate the analysts' dividend growth projections. I used Hagstrom's five- and ten-year DCF, the company's current earning power, and the valuation (PE PBV PS) price comparison average. What my model gave me is $37.90 a share, a possible 26.54% upside if met.

Now, please do not consider this as an expert advice or a buying tip for Sands China, or other companies that have been mentioned. Please do your own due diligence of the company if you are interested in buying their shares.

Disclosure: I have shares in the companies that have been mentioned above and would not engage in any transactions within the next 72 hours.

Reference

Crowe, P. (2015). Sheldon Adelson has to testify in a big court case against him and 'there's going to be mudslinging'. Retrieved fromwww.businessinsider.com/sheldon-adelson-...

Now, I find the ongoing crackdown on China's notorious big spenders temporary no matter how much publicity it gets. Continuous innovation to attract visitors such as the new casino project will still be ongoing (like the Parisian Macao at Cotai Strips, Macao "sometime" this 2016) and people (not only Chinese), but people around the Asian Region would still find Macao a wonderful tourist destination. Although there are only six licensed operators in the Macao Island who may operate the casino business, I find Sands China with the best fundamentals among its peers (see checklist above-of course with some exceptions). With 70.2% ownership by Las Vegas Sands (NYSE:LVS) I do not think LVS would let Sands China easily flop. Morningstar gave Sands China a four star with a narrow economic moat. According to Value Line, the recent plunge in Sands China brought down LVS's top line of about 25%. Despite this, they kept their 2018-2020 price projection of LVS in the $90-$130 a share versus its current market price of $50.90.

But my focus is still on the Sands China. The three challenges I find in this company in addition to the ongoing economic problem in Macao is its CEO succession, the ongoing lawsuit concerning an unfair dismissal of then former Sands China CEO Steven Jacobs, and the recent initiation of dividends.

I assume that a lawsuit can cause a lot and it may exacerbate the already struggling company, thus creating a perfect storm in the short term. First, Sheldon Anderson's age of 81 can be an alarming factor given his influence in both the LVC and Sands China operations. In addition, Edward M. Tracy, who was recently appointed as the Sands China's CEO in 2011, has decided to retire last March 7, 2015. He stated that there were no disagreements and only to serve as a consultant to the company then after. I am assuming the current interim president and executive director, Robert G. Goldstein, to be able to fulfill the CEO role anytime given his extensive experience in the casino-hotels business. I just find it interesting that in the midst of the allegations made by Steven Jacobs (former Sands China CEO) about Sheldon Anderson's approval of prostitution in his casino and blackmailing of high-ranking Macao officials (Crowe, 2015), which is ongoing for four and a half years already, Edward M. Tracy, appointed as Sands China CEO after Steven Jacobs departure, now retired at only the age of 62. Lastly, the company only started giving dividends in 2012. With this short dividend history with a 98.9 payout ratio ($1.71 billion USD according to its 2014 annual report) I am thinking whether or not to just rely on possible capital appreciation in the long term rather than on the attractive 6.18% it currently provides.

Alright, now I am going to use my valuation to see what is the fair value of Sands China. I average eight different models so as to obtain my own fair valuation of a company. To give better information on how I evaluate a company, here are some of the important data I use: Morningstar's key ratios, CAPM's method of determining the cost of equity, PE PBV PS average price, using only 2/3 (67%) analyst's dividend growth projections, using 2/3 of the company's current earnings power, using Hagstrom's five- and ten-year discount cash flow model, and using five, nine, and fifteen year (if applicable) dividend growth.

As you may observe, I value a stock based on their dividend history and growth. In this case, I am force to assume the reasonable growth of 21.37% forecasted by Yahoo Finance instead of the outrageous 752.80% forecasted by 23 analysts in The Financial Times. Let us remember that with the recent 2012 dividend issuance, the company has had a 22.37% dividend growth, a CAGR of 22.12%. In addition with the already north of 90 payout ratio, I personally do not think that this would be maintained for the long run or the payout ratio must at least be lessened to attain consistency.

Upon my calculation for the fair value of Sands China, I had to eliminate the analysts' dividend growth projections. I used Hagstrom's five- and ten-year DCF, the company's current earning power, and the valuation (PE PBV PS) price comparison average. What my model gave me is $37.90 a share, a possible 26.54% upside if met.

Now, please do not consider this as an expert advice or a buying tip for Sands China, or other companies that have been mentioned. Please do your own due diligence of the company if you are interested in buying their shares.

Disclosure: I have shares in the companies that have been mentioned above and would not engage in any transactions within the next 72 hours.

Reference

Crowe, P. (2015). Sheldon Adelson has to testify in a big court case against him and 'there's going to be mudslinging'. Retrieved fromwww.businessinsider.com/sheldon-adelson-...